Economic Evidence Base for London 2016

- This report provides an economic evidence base to help inform and support strategy development for London (see for example A City for All Londoners).

- It outlines how London’s economy has developed over time, the forces acting upon it, and identifies the risks and issues facing London’s economy. As such, the work covers a number of areas including: trade and London’s international competitiveness; the spatial characteristics of London; commuting and transport; land use and housing; the risks to London’s economy; London’s environment; people and the labour market; and some of the socio-economic issues faced by London.

- The report can be downloaded in its entirety but has also been split by chapter (see further below). Any comments on this publication can be sent directly to GLA Economics: [email protected]

Executive summary

The economic evidence base seeks to provide consistent data and analysis of London’s economy for strategy development purposes (for instance to support the development of the London Plan, Economic Development Strategy and Transport Strategy). The executive summary provides a condensed outline of the main findings.

On many measures London’s economy is very successful. In 2014 London’s economic output (its ‘Gross Value Added’) totalled £364 billion; twice the size of the economies of Scotland and Wales put together.

Indeed if London’s economy is considered against European countries (on a comparable basis) it would rank as the eighth biggest economy; London’s economy is larger than Belgium, Sweden, Austria or Norway for example.

Size of European economies and London (2014) Million PPS (purchasing power standard)

Source: Eurostat. Note, PPS is an artificial currency unit used to compare countries or cities, on a consistent basis: one PPS can buy the same amount of goods and services in each country.

London’s economic success is further illustrated by the fact that, contrary to the country as a whole, London runs a trade surplus with the rest of the world. As a result, London’s economy provides a net injection to the national economy which, through supply chain linkages, helps to drive economic activity across the country. The more international trade London engages in the more economic activity there is likely to be for the rest of the UK.

International trade is an important influence on London’s economy because it increases the size of the market into which London’s businesses can sell (or buy from): the bigger the market, the more economically viable it is to focus on specialised products or services.

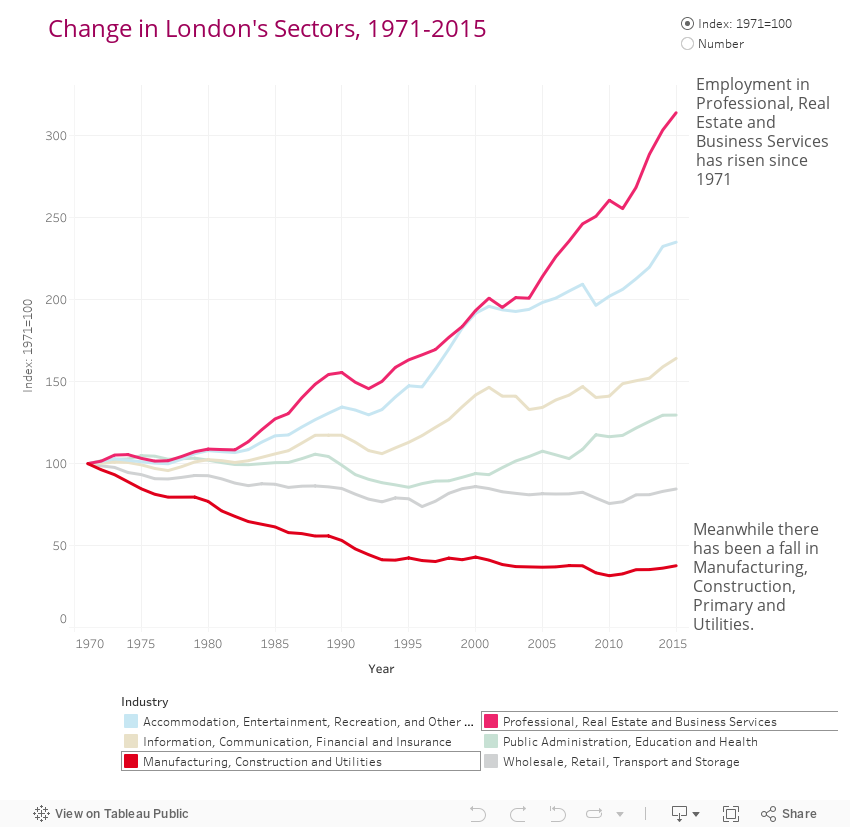

As a result, globalisation - the increasingly connected and integrated nature of the international economy - has led to structural change in London’s economy – with London specialising in a number of internationally competitive business areas (see chart showing change in London's sectors, 1971-2015).

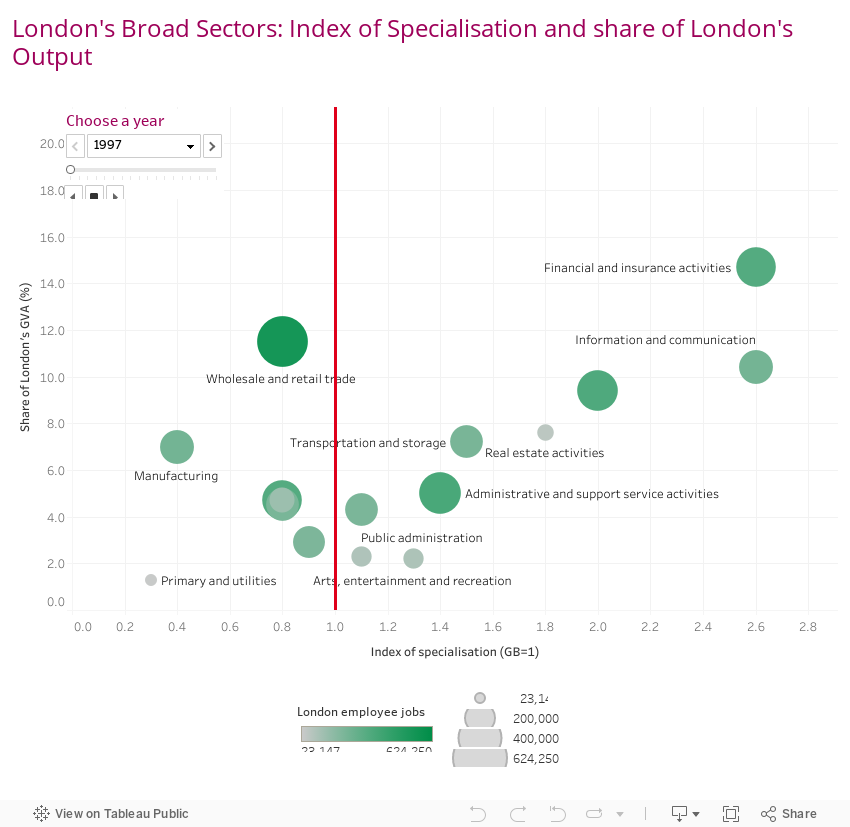

London’s economy is specialised (in the sense that it has a greater proportion of employment in a particular sector when compared to the rest of the country) in financial and insurance activities and this is also London’s biggest area of economic activity (accounting for almost a fifth of London’s GVA and over 4 per cent of the entire UK’s economic output).

Similarly, London is specialised in information and communication, professional services and real estate – which together account for another third of London’s economic activity. What the chart below shows is that, unsurprisingly, London is not specialised (in relation to the rest of the country) in activities that might be considered to be land-intensive, like agriculture and traditional manufacturing.

Index of specialisation is calculated as follows: (sector employee jobs in London / all employee jobs in London) / (sector employee jobs in Rest of GB / all employee jobs in Rest of GB).

Many of the sub-sectors within the broad sector headings outlined in Figure 1 are internationally competitive specialisms – where London exports a significant amount of services. Some examples include air transport; film/TV/music; creative, arts and entertainment activities; computer programming and consultancy; finance (e.g. securities and fund management activities); legal and accounting services; and, advertising – all of which have a significant concentration in London (as compared to the rest of the country).

More detail on London’s trade and specialisation is provided in Chapter 1 of the evidence base.

This sectoral specialisation has also, to a degree, manifest itself in a spatial specialisation or concentration. So particular (and many) functions of London’s economy have tended to locate in certain areas of London – primarily central London.

This is because central London offers a number of features that can’t be found in combination in many other places in the UK or the world over. London is an attractive location for international businesses given its well-established legal, political and regulatory frameworks; the use of the English language as a means of international communication; international transport links; and, a low rate of corporation tax amongst other factors.

This attractiveness to business is highlighted in many global city ranking indices (for instance ranking as the leading global city according to the PWC Cities of Opportunity and the Global Financial Centres Index). Indeed 40 per cent of the world’s largest 250 companies base their European headquarters in London. Moreover, central London additionally offers businesses good access to a deep and highly-skilled labour force.

Central London also offers a range of complementary markets (both in terms of businesses able to serve or supply (input markets) and businesses willing to buy the product or service (output markets)) and the benefits of spill-over effects such as the rapid transfer of innovation and knowledge. These so-called “agglomeration benefits” bring benefits to the economy over and above those that accrue to the individual firms themselves.

As a result, whilst the UK and London offers an attractive base for many businesses, central London has a particular attraction for many globally competitive firms who want to locate near to one another.

The attractiveness of London to global businesses means there are many internationally attractive employment opportunities available in London – one of the factors which encourages people to live in the capital. However, other factors also make London an attractive place for people to live and work. These can include London’s culture and heritage; the access to green space in London; and, access to good quality schools and health care.

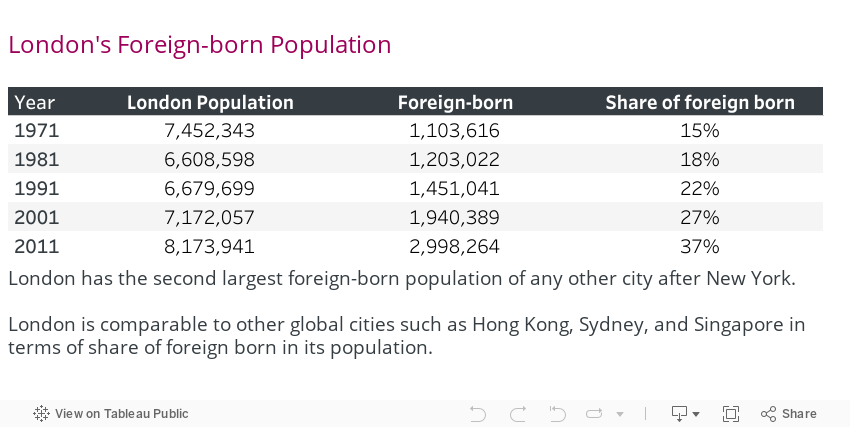

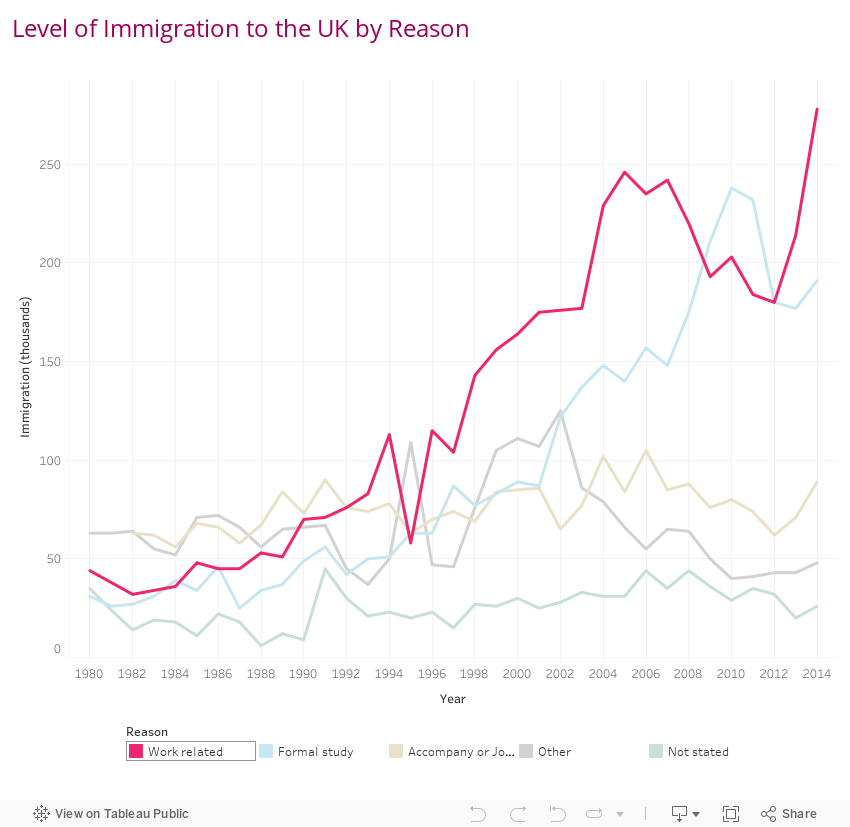

London’s attractiveness to people is evidenced by its population growth in the recent past, with London’s population growing by an average of around 95,000 a year since 2000 (and consistently over 100,000 a year since the economic downturn of 2008/09). Much of this increase has been from international migration – making London a very diverse city with 37 per cent of the population born overseas.

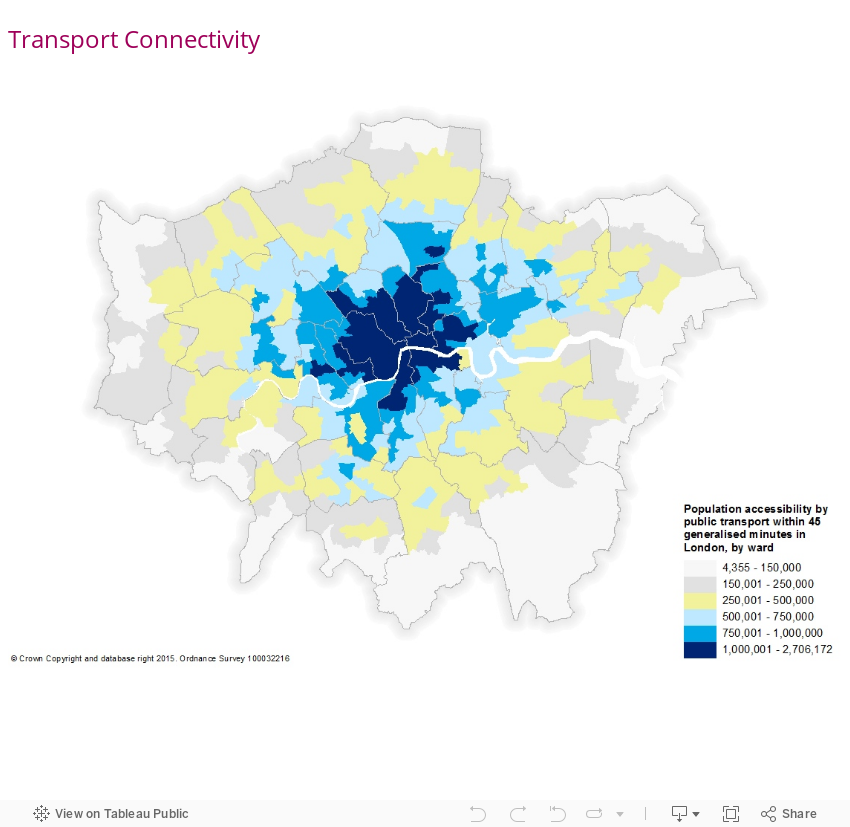

The visualisation below shows the number of people who, using public transport and a 45-minute travel time, could travel to individual wards within London. It shows that up to 2.7 million people could get to the areas marked in dark blue within 45 minutes. This illustrates the attractiveness of central London to businesses particularly reliant on skilled labour; London’s radial transport system opens up a huge labour market to firms located in central London.

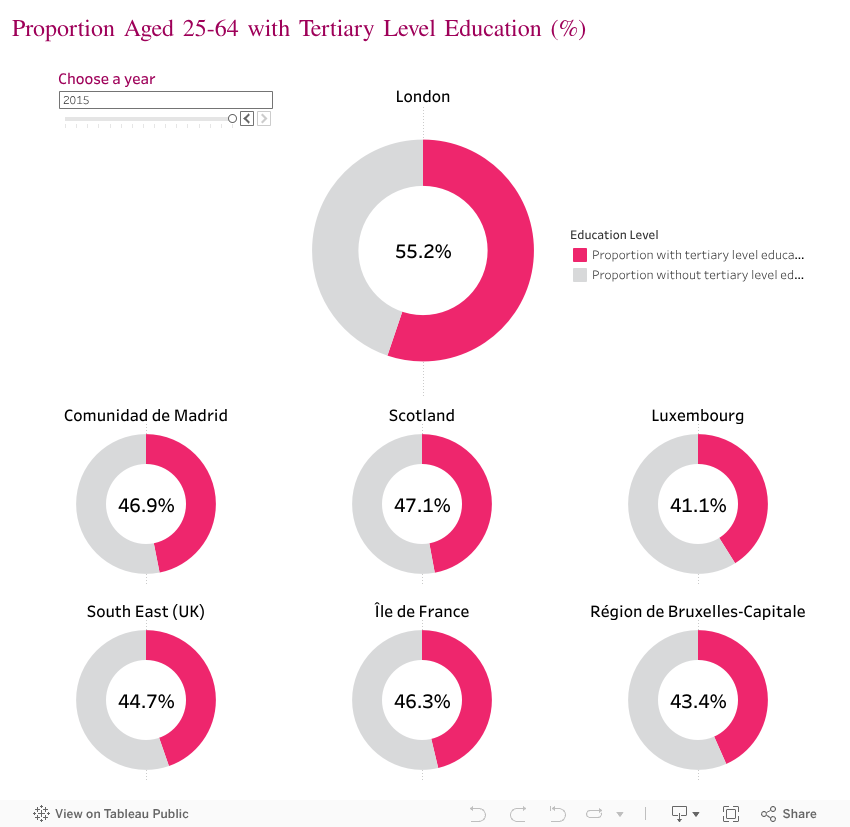

Many of these workers will also come from outside London’s boundaries principally from the Greater South East. Indeed in some parts of the Greater South East, London accounts for the place of work for over 40 per cent of that area’s total workforce. As a result, London is a highly-skilled city with over half of all workers in the capital educated to at least degree level.

The product of all these factors is a concentration of employment at the centre of the city. The chart below shows the number of employees per square km. In essence the preference revealed by companies’ business location decisions is that they want to locate near the centre – near to one another – in order to benefit from central London’s agglomeration benefits.

These agglomeration benefits further underpin London’s international comparative advantage with research suggesting that the areas in which London specialises – such as financial and business services - are those areas that benefit most from agglomeration economies.

This competition for space in the centre of London puts upward pressure on the price of land and means businesses in London have to be very competitive to survive. This competition drives productivity which is reflected in ONS productivity figures showing that London’s economy is around 30 per cent more productive than the UK average.

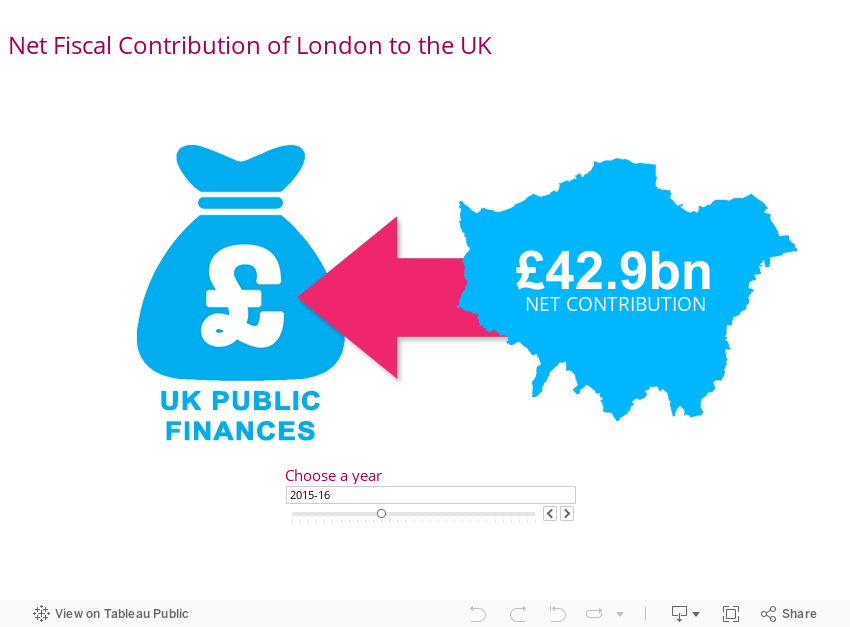

This productivity, trade and general level of economic activity also drives significant fiscal surpluses. In 2013-14 it is estimated that London raised £34 billion more in taxes than was spent in London from public expenditure.

This is the highest amount of any region or country of the UK (with the South East and East of England the only other regions to make a positive contribution to the Exchequer). To put this figure in context, public deficits are usually represented as a proportion of annual GVA/GDP. In 2013-14 London’s net fiscal surplus was equivalent to around 10 per cent of London’s GVA, at a time when public sector net borrowing for the UK as a whole was running at almost six per cent of GDP.

Indeed despite the economic downturn in 2008-09 London continued to generate a fiscal surplus for the country as a whole – and has done for at least the past two decades or so. More detail on London’s spatial economy and the competition for land is provided in Chapters 2 to 4 in the evidence base.

However, London’s economy is about more than central London alone. Indeed, whilst many of the globally competitive businesses that locate in the very centre of the city (to access a large pool of highly-skilled labour and to feed off one another to do business), other sectors - particularly those serving local markets - need to be located near to consumers.

These sectors (e.g. retail, health, education, local government etc) tend to have their employment spread much more widely across London – providing local employment opportunities for London’s residents. Indeed the majority of London’s employment is located outside central London – spread across London as a whole.

As noted earlier, London’s attractiveness as a place to live and work is illustrated by the growth in its population in recent decades. London’s population now stands at 8.7 million, the highest it has ever been and more than Scotland and Wales put together (despite London accounting for just 1.6 per cent of the combined land area of Scotland and Wales).

This population drives a significant level of demand for a wide range of locally delivered goods and services: retailers to supply the food and goods required to live; teachers to teach London’s schoolchildren; health care professionals to run London’s hospitals, GP surgeries and care services for example. Central London businesses also drive a demand for goods and services that are, in part, serviced by businesses located in the rest of London.

This level of demand means that a significant number of people are employed in London in these sectors. Over half a million people in London are employed in health and social work activities. Similarly, over 400,000 people in London are employed in the retail and education sectors respectively.

As such these three sectors each employ more people in London than are employed in London’s financial and insurance services. In all, London employs more than 200,000 people in 13 different broad sectors; London is a diverse economy.

Projections for London’s population and employment suggest London will continue to grow over the next few decades although there are upside and downside risks to these projections. One of the main potential future influences on these projections is the final outcome from the referendum vote to leave the European Union (EU).

The nature and scale of any long-term impact from the vote is unknown at the moment and will depend to a large extent on factors like the trade deals that are negotiated with the EU and non-EU countries and any change to the UK’s existing migration system (including the free movement of labour within the EU). More detail on the projections and the numerous risks to those projections are set out in Chapter 6 of the evidence base.

As shown above, central London is a hub for global business services: generating significant levels of employment, substantial levels of service exports together with considerable fiscal surpluses for the UK as a whole. However, this evidence base sets out a number of risks to London’s future economic prosperity. If these risks are not mitigated then central London risks losing its attractiveness to both business and people, which could in turn erode the agglomeration benefits.

Ultimately this would result in London losing its international competitiveness, with businesses choosing to move their premises not to elsewhere in the UK, but to another country. If this were to happen the UK would lose the employment, exports, spur to productivity and significant fiscal surpluses that are currently generated by central London businesses; this would be a loss to the UK as a whole, not just to London.

In essence, London’s success and its attractiveness to businesses and people bring about a number of issues that need management if London is to continue to prosper.

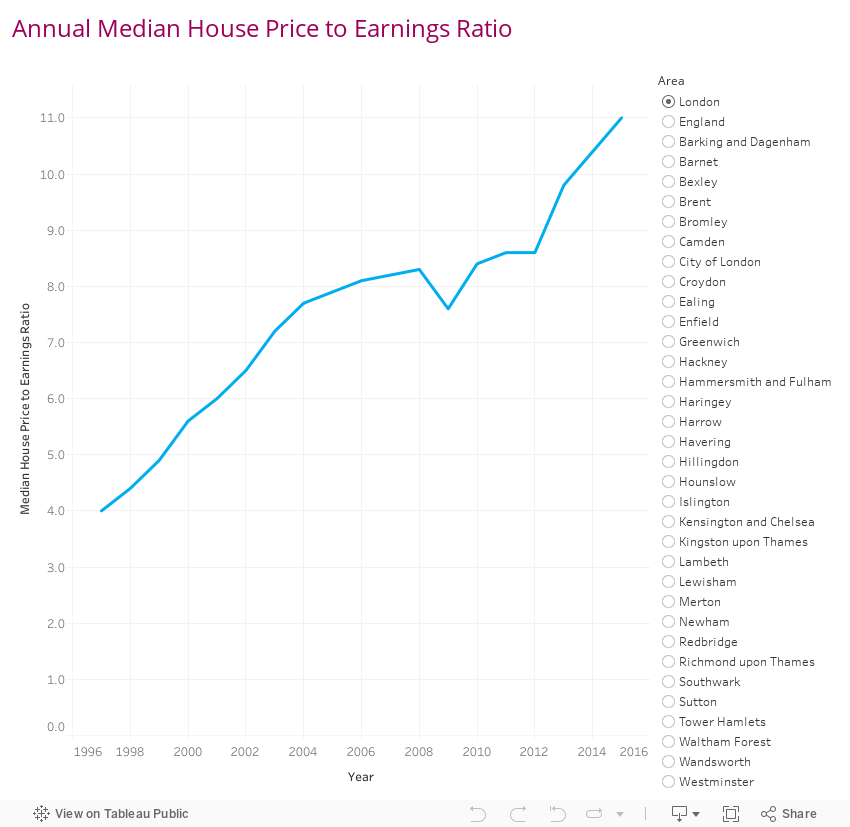

The number of people and businesses that want to locate in London means there is intense competition for land in London which results in some of the highest land and property prices in the UK and across other global cities. Over the past couple of decades or so there have been strong rises in London house prices which are far higher than the rest of the country.

The gap in average house prices between London and the rest of the country has grown wider every year since 1995 with the exception of 2009. House prices are, on average, over 10 times average earnings in London and therefore represent a significant barrier to many Londoners looking to own their own home in London.

High house prices also knock on to high rental prices with the relative costs of private renting having risen sharply in London compared to other English regions in the past decade or so. Such high housing costs – high by international, not just domestic, standards - reduce the affordability of London.

Whilst London’s population has continued to rise in the past few decades, there is a risk that the affordability of London reduces to such an extent that London loses its attractiveness as a place to live and businesses find it increasingly difficult to fill the vacancies they have.

There is also a risk that high demand for housing may crowd out commercial (including industrial) uses of land. Evidence from the London Development Database suggests that Permitted Development Rights introduced in May 2013, which allow conversion of offices to housing without the normal planning procedures, are having a considerable impact on the stock of office space in some boroughs.

In the period 2008 to 2013 the percentage of residential units completed on land classed previously as office use was around 12 per cent, but in 2014/15 this increased to 24 per cent. Similarly to population, whilst the number of businesses located in London has continued to increase over at least the last decade or so (with the exception of 2008/09), there is a risk that business premises become too expensive such that businesses no longer find it profitable to operate in London.

The economic evidence base highlights a number of other, what may be considered as, ‘congestion costs’ which, if left unchecked or unmanaged, could risk London’s future attractiveness to both business and people.

One such cost derives from the pressures on London’s transport network. Many parts of London’s private and public transport networks suffer from significant congestion and overcrowding; London also has limited airport capacity. There are similar pressures in other parts of London’s infrastructure network.

London’s significant population growth has put a strain on many public services including school places, health services and social housing for example. London’s growth is estimated to increase overall energy demand by 20 per cent by 2050.

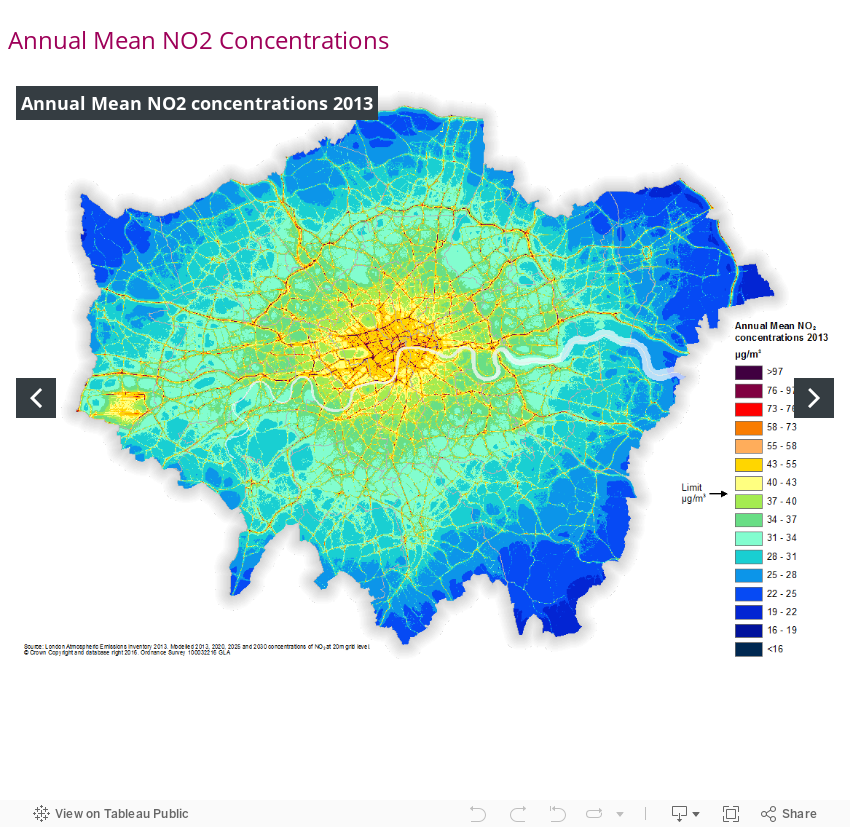

Moreover, without intervention it is predicted that London will have a deficit in water supply of half a billion litres of water per day by 2050. London’s growth also puts significant pressure on its natural capital – those elements of the natural environment which provide goods and services. Issues like air pollution, noise disturbance, flooding and climate change more generally all pose risks to London’s future growth (see Chapter 7 for more detail).

And for all its apparent success in terms of economic output, trade and tax raising potential, not everyone benefits equally from London’s prosperity.

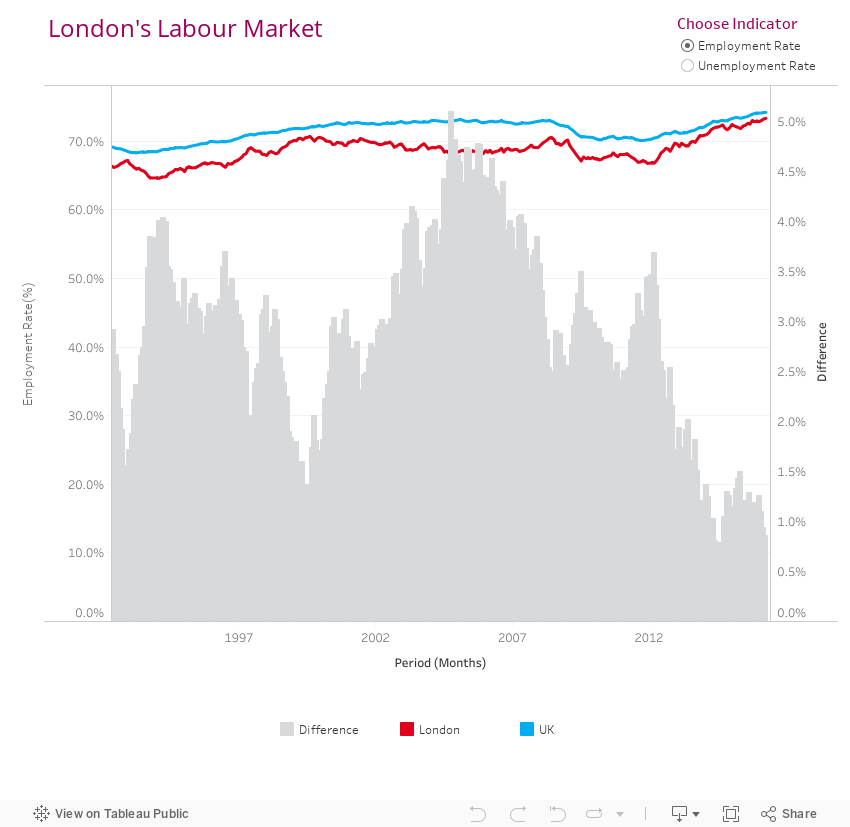

Whilst London’s employment rate is currently at the highest level it has been since at least 1992, it remains below that for the UK as a whole.

Women with dependent children in London in particular are less likely to be in employment than their counterparts in the rest of the country. London’s unemployment rate is also higher than that for the UK as a whole.

Between 2008 and 2015 London’s nominal median gross hourly wage increased by 8.4 per cent. This was the slowest rate of increase across all 12 UK regions (with the average rate of growth 11.5 per cent for the UK). This coupled with the rise in costs over the same period, with increases in housing costs, transport costs, childcare costs and fuel costs have all combined to reduce the affordability of living in London in recent times.

Indeed almost half of London households have less disposable income, after accounting for housing costs, than equivalent households in the rest of the UK. London’s labour market performance is considered in Chapter 9 of the evidence base with London’s socio-economic issues considered in detail in Chapter 10.

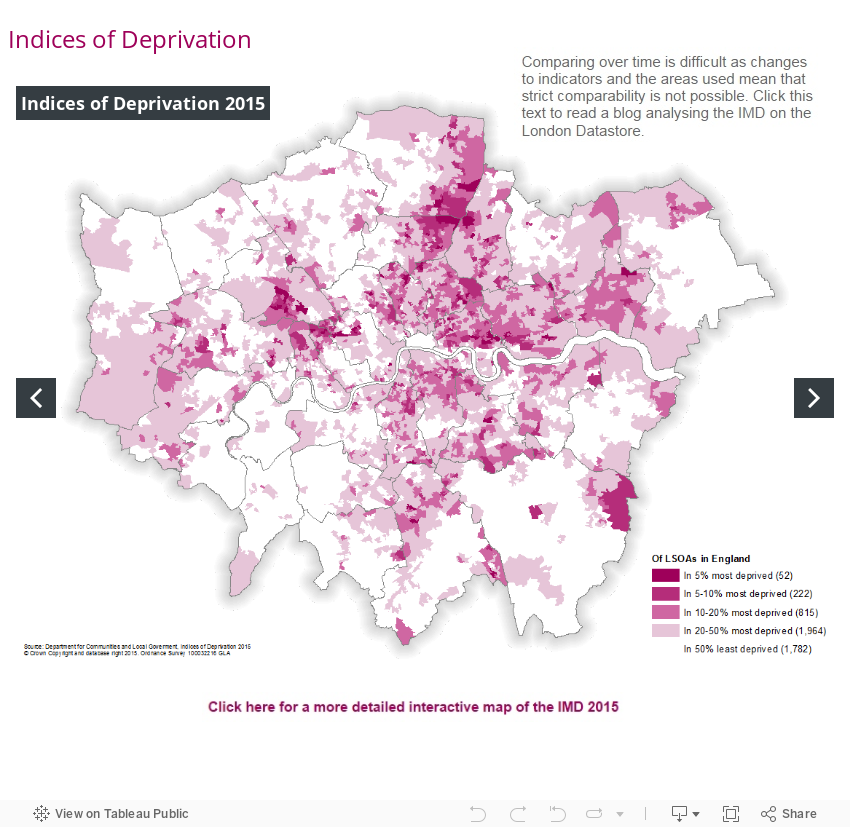

Poverty levels among London’s population, after taking account of housing costs, are much higher in London than the UK as a whole.

Up to a third of all inner London residents are in poverty on this measure and nearly a quarter of outer London residents, which is also higher than for any other UK region. The situation is even more acute for child poverty; 46 per cent of households with children are in poverty in inner London and 33 per cent in outer London (the highest rates of any UK region).

There is a correlation between socio-economic inequalities and health inequalities in London; health outcomes differ between different population groups and by location as well as when broken down by educational attainment, housing tenure and employment status. To this end, London faces certain health issues that are unique in England.

Around two fifths (43 per cent) of all people living with diagnosed HIV in the UK live in London, and London accounts for two fifths of all tuberculosis cases in England. Many Londoners are also affected by a mental health disorder, with two million people in the capital estimated to experience some form of mental ill health every year.

On average, Londoners reported the lowest levels of life satisfaction, happiness and feeling the things they do in life are worthwhile and the highest anxiety rating of any UK region. In 2015/16, London’s average anxiety rating was 3.04 (out of 10) - significantly higher than the England average of 2.87 in statistical terms.

Londoners rated themselves as feeling relatively less satisfied with their life nowadays – giving an average score of 7.51 out of 10, again significantly lower than the UK average of 7.65 statistically speaking. These average figures can however mask differences in the share of respondents who report low levels of personal wellbeing (or high levels of anxiety) that may be of particular concern.

So whilst, on many measures, London is a very successful economy, there are many risks to London’s future economic prosperity and instances where London residents are not benefitting from London’s economic success. The body of the evidence base considers these issues in more detail.

Chapters 1 - 10

You can also download Chapters on relevent areas you'd like to explore further.

Need a document on this page in an accessible format?

If you use assistive technology (such as a screen reader) and need a version of a PDF or other document on this page in a more accessible format, please get in touch via our online form and tell us which format you need.

It will also help us if you tell us which assistive technology you use. We’ll consider your request and get back to you in 5 working days.